Planning a home renovation in 2026? The Home Depot Credit Card offers special financing on large purchases, but approval depends on your credit score and financial profile. In this complete guide, you’ll learn the credit score needed, key benefits, interest rates, approval tips, and whether this card is worth it before you apply.

Quick Verdict (2026)

| If You Want… | Choose |

| Project financing at Home Depot | Home Depot Credit Card |

| Everyday 5% store discount | Lowe’s Advantage Card |

| Cashback everywhere | General Cashback Card |

| Long 0% intro APR | Bank-issued rewards card |

What Is the Home Depot Credit Card?

Home Depot Credit Card Overview (2026)

| Feature | Details |

| Card Type | Store Credit Card |

| Issuer | Citibank |

| Annual Fee | $0 |

| Recommended Credit Score | 640+ (Fair to Good) |

| Special Financing | 6 Months on $299+ Purchases |

| APR | High Variable APR (If Balance Not Paid in Full) |

| Rewards Program | No Traditional Cashback Rewards |

| Store Usage | Only at Home Depot |

| Instant Approval | Often Yes (Online & In-Store) |

| Credit Reporting | Reports to Major Credit Bureaus |

Here’s a quick overview of the Home Depot Credit Card before we go into full details.

The Home Depot Credit Card is a store-only credit card designed for customers who frequently shop at The Home Depot for home improvement projects. It allows cardholders to finance large purchases and manage renovation expenses more easily through special promotional financing offers. For instance, you could use the card to finance a $1,500 appliance purchase and take advantage of the special financing period to pay it off over time.

Consider a DIY homeowner planning a complete kitchen remodel over several months: they might use the card for staggered purchases, such as cabinets, flooring, and a new refrigerator, taking advantage of promotional financing on each large order and spreading payments without immediate interest. Alternatively, a general contractor managing multiple renovation jobs might use the card to purchase building supplies and tools in bulk for different clients. The extended return period and flexible financing can help the contractor handle cash flow, keep projects running smoothly, and manage expenses until client payments are received. These varied scenarios show how both individual homeowners and contractors can benefit from using the Home Depot Credit Card for different home improvement needs.

Instead of offering traditional cashback rewards, this card focuses primarily on deferred-interest financing. Eligible purchases (typically $299 or more) qualify for promotional financing, giving customers time to pay off larger expenses without immediate interest charges—if paid in full within the promotional period.

The card can be used for in-store and online purchases at Home Depot, making it suitable for buying appliances, tools, building materials, flooring, and renovation supplies. It is especially helpful for homeowners planning remodeling projects or contractors managing short-term material costs.

Because it is a retail store card, it is intended for use exclusively at Home Depot and is best suited for shoppers who regularly make large home improvement purchases and can repay balances within the promotional period.

Home Depot Credit Card Benefits and Rewards

The Home Depot Credit Card is built primarily around financing flexibility rather than traditional cashback rewards. It is ideal for customers planning medium to large home improvement purchases.

1. 6-Month Special Financing on $299+

Cardholders receive 6 months of deferred interest financing on purchases of $299 or more. This allows you to spread out payments over time without paying interest — as long as the full balance is paid before the promotional period ends.

During special promotions, extended financing options such as 12, 18, or even 24 months may be offered on qualifying purchases.

2. No Annual Fee

The card does not charge an annual membership fee, making it cost-effective for occasional or project-based use.

3. Exclusive Cardholder Promotions

Home Depot occasionally provides:

- Special seasonal financing offers

- Limited-time discounts

- Project-based promotional plans

These offers are typically available only to cardholders.

4. Extended Return Period

Cardholders may receive a longer return window compared to standard purchases, which is helpful when managing renovation timelines.

5. Large Purchase Flexibility

The card is particularly useful for:

- Appliances

- Flooring projects

- Kitchen remodels

- Bathroom upgrades

- Tools and building materials

It allows homeowners and contractors to manage short-term cash flow during renovations.

Important Note About Rewards

Unlike many traditional credit cards, the Home Depot Credit Card does not offer ongoing cashback or travel rewards. Its primary value lies in financing benefits rather than reward accumulation.

Interest Rates, Fees & Deferred Interest Explained

Before applying for the Home Depot Credit Card, it is important to understand how interest and fees work — especially the deferred interest feature.

Current APR (Variable Rate)

The Home Depot Credit Card typically carries a high variable APR (often above 25%). (Home Depot Credit Card Editor’s Review for January 2026, 2026) This rate applies to any balance not paid within the promotional financing period.

Because the APR is relatively high compared to general-purpose credit cards, this card is best used for short-term financing rather than carrying long-term balances.

How Deferred Interest Works

The card offers deferred interest financing, not a true 0% APR card.

Here’s what that means:

- If you make a qualifying purchase (usually $299 or more), you may receive 6 months of promotional financing.

- If you pay the full balance before the promotional period ends → you pay no interest.

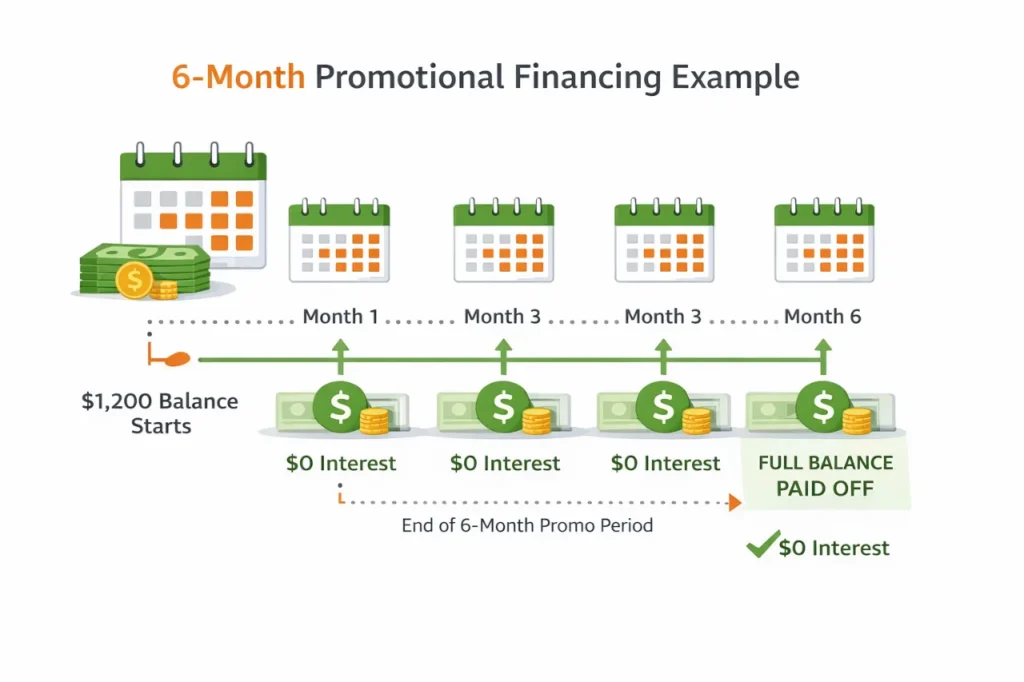

- If even $1 remains unpaid after the promotional period, interest is added retroactively to the entire original purchase amount from the purchase date. For example, if you make a $1,200 purchase with a 6-month deferred interest offer and still owe $50 when the promotion ends, you could be charged interest on the full $1,200 for the entire 6 months, not just the $50 unpaid portion. This could add up to more than $150 in interest, depending on the APR. To avoid this costly mistake, consider setting calendar reminders a few days before your promotional period ends, enrolling in autopay for the full statement balance, or splitting payments into automatic monthly installments to match your budget. You can also use the Home Depot mobile app, which offers payment notifications, or sign up for account alerts through your online card portal so you receive reminders about upcoming due dates or expiring promotional periods. These strategies can help ensure you pay off your balance on time and steer clear of unexpected interest charges.

This is why paying off the full balance before the deadline is critical.

Late Payment Fees

If you miss a payment, you may be charged:

- A late payment fee

- Interest on the unpaid balance

- Potential damage to your credit score

Setting up automatic payments can help avoid late fees.

Other Potential Fees

- Returned payment fee (if a payment bounces)

- No annual fee

- No foreign transaction usage (card is store-only)

Is the Interest Rate Worth It?

The high APR makes this card risky for long-term balances. However, if you consistently pay off purchases within the promotional financing window, you can avoid interest entirely and benefit from short-term flexibility.

Financing Example Calculation Table

Financing Example: How Deferred Interest Works

Scenario: $1,200 Appliance Purchase (6-Month Promo)

| Scenario | What You Pay | Interest Charged |

| Paid in full within 6 months | $1,200 | $0 |

| $100 remaining after 6 months | $1,200 + retroactive interest | Interest added on full $1,200 |

| Minimum payments only | Balance remains | High interest applied after promo |

What Credit Score Is Needed for Home Depot Card Approval?

To qualify for the Home Depot Credit Card, most applicants typically need a fair to good credit score, generally around 640 or higher. While there is no officially published minimum income requirement, applicants are usually expected to demonstrate a steady source of income that shows an ability to repay new credit. In most cases, a yearly income of at least $15,000 to $20,000 is considered sufficient for approval, although higher income levels may increase your chances of being approved or qualifying for a larger credit limit.

While approval is not based on credit score alone, having a score in this range significantly improves your chances.

Applicants with a credit score of 640 or above generally have stronger approval odds, while scores below 600 often face a higher risk of denial. Approval decisions may also depend on factors such as income, existing debt, recent inquiries, and overall credit history.

Credit Score Guidelines

- 720+ (Excellent): Very high approval odds

- 680–719 (Good): Strong approval chances

- 640–679 (Fair): Moderate approval chances

- Below 620: Higher risk of denial

Keep in mind that these are general approval trends, not guaranteed thresholds.

Other Factors That Affect Approval

In addition to your credit score, the issuer also reviews:

- Your income level

- Debt-to-income ratio

- Existing credit card balances

- Recent hard inquiries

- Length of credit history

- Payment history

Even with a 640+ score, high debt or multiple recent applications could reduce approval chances.

Does the Home Depot Credit Card Help Build Credit?

Yes. The card reports to major credit bureaus. If you:

- Pay on time

- Keep utilization low

- Avoid missed payments

It can help strengthen your credit profile over time.

Tip Before Applying

Check your credit score before submitting an application. If your score is close to 640, improving it slightly before applying may increase your approval odds and potentially your credit limit.

How to Apply for the Home Depot Credit Card (Online & In-Store)

Applying for the Home Depot Credit Card is simple and can be done online or in-store.

Option 1: Apply Online

You can apply through the official website of The Home Depot by following these steps:

- Visit the Home Depot credit services page.

- Click “Apply Now”

- Fill in your personal details (name, address, income, SSN)

- Submit your application

In many cases, applicants receive an instant decision within minutes.

Option 2: Apply In-Store

You can also apply at checkout inside a Home Depot store. A store associate can guide you through the application process. Approval decisions are often provided immediately.

When applying in-store, be prepared to bring a government-issued photo ID (such as a driver’s license), your Social Security Number, proof of income (for example, a pay stub or recent tax document), and your current address. Arriving with this information can help your application go smoothly and avoid delays.

Basic Eligibility Requirements

To qualify, you generally must:

- Be at least 18 years old (19 in some states)

- Have a valid Social Security Number.

- Provide proof of income.

- Have a U.S. residential address.

Approval depends on creditworthiness and financial profile.

What Happens After Approval?

If approved:

- You may receive a temporary shopping pass for immediate use.

- Your physical card will arrive by mail within 7–10 business days.

- You can start using promotional financing immediately.

Tips Before Submitting Your Application

- Check your credit score first.

- Pay down existing balances if possible.

- Avoid applying for multiple credit cards at once.

- Ensure your income details are accurate.

Taking these steps can improve your approval chances and potentially increase your starting credit limit.

Common Reasons for Denial & What to Do Next

If your Home Depot Credit Card application is denied, don’t panic. Many applications are declined due to financial factors.

Common Reasons for Denial

1. Low Credit Score

A score below the recommended range (typically under 640) can reduce approval chances.

2. High Credit Utilization

If you are using more than 30–40% of your available credit limits, lenders may view you as high risk.

3. Too Many Recent Applications

Multiple hard inquiries within a short period can negatively impact approval decisions.

4. High Debt-to-Income Ratio

If a large portion of your income is already committed to debt payments, it may signal repayment risk.

5. Limited Credit History

A very short credit history or lack of active accounts can make approval more difficult.

6. Recent Late Payments

Missed or late payments significantly lower approval odds.

What To Do After a Denial

If your application is declined, here are the smart next steps:

1. Review the Adverse Action Letter

You will receive a letter explaining the specific reason for denial. Use this to understand what needs improvement.

2. Check Your Credit Report

Review your credit report for errors or inaccuracies and dispute any incorrect information.

3. Lower Your Credit Utilization

Pay down existing balances to below 30% of your total credit limit.

4. Improve Payment History

Make consistent, on-time payments for at least 3–6 months before reapplying.

5. Wait Before Reapplying

Avoid submitting another application immediately. Give your credit profile time to improve.

Can You Reapply?

Yes, but it’s better to wait until your credit score improves and your financial profile looks stronger. Reapplying too soon may lead to another hard inquiry and another denial.

How to Improve Your Credit Score Before Applying

If your credit score is slightly below the recommended range, improving it before applying can significantly increase your approval chances.

Even small improvements (20–40 points) can make a difference.

1. Lower Your Credit Utilization

Credit utilization is one of the biggest factors affecting your score.

- Keep balances below 30% of your total credit limit.

- Ideally, aim for under 10% for the best results.

- Pay down revolving credit card balances first.

Lower utilization can quickly improve your score within 30–60 days.

2. Make All Payments On Time

Payment history is the most important credit scoring factor.

- Never miss a due date.

- Set up automatic payments.

- Pay at least the minimum due.

Consistent on-time payments over several months can steadily boost your score.

3. Avoid Multiple Hard Inquiries

Each credit application creates a hard inquiry, which may temporarily lower your score.

Avoid applying for:

- New credit cards

- Personal loans

- Store financing

Wait at least 3–6 months before submitting another credit application.

4. Check Your Credit Report for Errors

Sometimes your score may be affected by incorrect reporting.

Review your credit report for:

- Incorrect late payments

- Duplicate accounts

- Fraudulent activity

Disputing errors can lead to score improvements.

5. Increase Your Credit Limit (If Possible)

If you have existing credit cards in good standing, requesting a credit limit increase (without a hard pull) can reduce your utilization ratio and improve your score. With the Home Depot Credit Card, you can usually request a credit limit increase after several months of responsible use, such as making consistent on-time payments and maintaining low balances. You can request a limit increase by logging into your Home Depot Credit Card account online or by calling customer service. Approval will depend on your payment history, creditworthiness, and current income details.

When approved, typical starting credit limits for the Home Depot Credit Card usually range from $500 to $2,500, although some applicants may be approved for slightly higher or lower amounts based on their credit profile and income. Knowing your likely starting limit can help you plan for large purchases and set expectations for what you can finance.

Increasing your credit limit can help improve your credit utilization rate and may give you more flexibility for larger purchases in the future.

6. Build Positive Credit Activity

If your credit history is limited:

- Keep older accounts open.

- Use a small recurring charge and pay it off monthly.

- Maintain active, responsible credit usage

How Long Should You Wait Before Reapplying?

If denied, waiting 3–6 months while improving your credit profile is usually a smart strategy before trying again.

Improving your financial stability first increases your chances of approval and may even help you qualify for a higher credit limit.

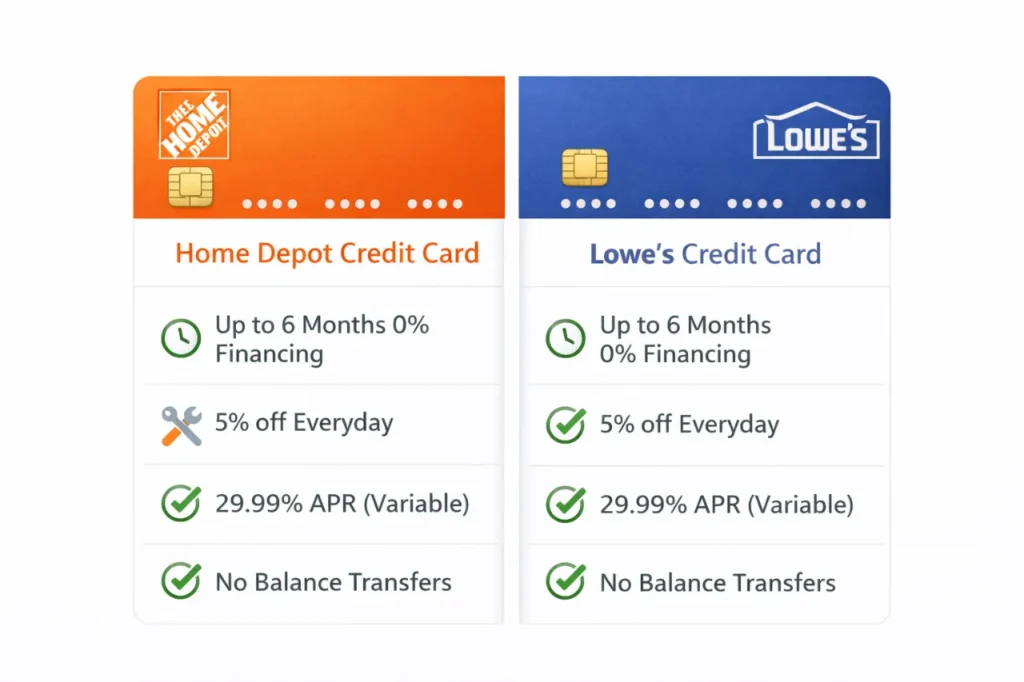

Home Depot vs Lowe’s Credit Card Comparison

If you frequently shop at home improvement stores, you may be deciding between the Home Depot Credit Card and the Lowe’s Advantage Card. Both are store-only credit cards, but their benefits differ slightly.

Financing Options

Home Depot Credit Card

- 6-month deferred interest financing on purchases of $299+

- Occasional extended promotional financing (12–24 months during special events)

Lowe’s Advantage Card

- Option for 5% discount on eligible purchases

- Or special financing promotions (varies by purchase amount)

If you prefer spreading payments over time, Home Depot’s financing structure may appeal more. If you prefer instant savings on every purchase, Lowe’s 5% discount can be attractive.

Rewards Structure

- Home Depot focuses primarily on financing rather than cashback.

- Lowe’s offers an everyday 5% discount option instead of traditional rewards points.

Neither card provides travel rewards or general cashback like major bank credit cards.

APR & Fees

Both cards typically have:

- High variable APR

- No annual fee

- Deferred interest on promotional financing

Because of the high APR, both cards are best used for short-term financing and paid off before interest applies.

Store Usage

Both cards are store-specific and can only be used at their respective retailers and websites.

Which One Is Better?

Choose the Home Depot Credit Card if:

- You make large renovation purchases.

- You prefer promotional financing flexibility.

Choose the Lowe’s Advantage Card if:

- You want immediate savings with a 5% discount.

- You shop frequently for smaller purchases.

Your decision should depend on your shopping habits and repayment strategy.

Home Depot vs Lowe’s Credit Card (2026 Comparison)

| Feature | Home Depot Credit Card | Lowe’s Advantage Card |

| Store | Home Depot | Lowe’s |

| Card Type | Store-Only Credit Card | Store-Only Credit Card |

| Annual Fee | $0 | $0 |

| Recommended Credit Score | 640+ (Fair–Good) | 640+ (Fair–Good) |

| Standard Financing | 6 Months on $299+ | 6 Months on $299+ (varies) |

| Everyday Discount | No | 5% Off Eligible Purchases |

| Extended Financing Offers | Yes (12–24 months promos) | Yes (Special promos) |

| APR | High Variable APR | High Variable APR |

| Usable Outside Store | No | No |

| Best For | Large project financing | Everyday savings |

How to Login, Check Balance & Manage Your Account

Managing your Home Depot Credit Card account is simple through the online account portal. Regular account monitoring helps you avoid late payments and stay within your promotional financing deadlines.

Login Process

To access your account:

- Visit the official credit card login page on The Home Depot website.

- Enter your User ID and Password

- Click “Sign In”

If you are a new cardholder, you’ll need to register your card before accessing online services.

How to Check Your Balance

After logging in, you can:

- View your current balance.

- Check available credit

- Review recent transactions

- Monitor promotional financing expiration dates.

Tracking your balance is especially important if you are using deferred interest financing.

Payment Options

You can make payments through:

- Online account dashboard

- Automatic monthly payments (Autopay)

- Phone payments

- Mail payments

Setting up autopay can help prevent missed due dates and late fees.

Paperless Statements

Cardholders can opt into paperless billing to:

- Receive digital monthly statements.

- Track spending more easily

- Reduce paper clutter

Where You Can and Cannot Use the Card

The Home Depot Credit Card can be used:

- At Home Depot retail stores

- On the official Home Depot website

It cannot be used at other retailers, restaurants, or online platforms outside Home Depot.

Fraud Protection & Security

To protect your account:

- Monitor transactions regularly

- Report suspicious activity immediately.

- Use strong passwords

- Enable account alerts if available.

If your card is lost or stolen, contact customer service immediately to prevent unauthorized charges.

Pros and Cons of the Home Depot Credit Card

Home Depot Credit Card Pros and Cons

| Pros | Cons |

| No annual fee | High variable APR |

| 6-month financing on $299+ | Deferred interest risk |

| Occasional extended promo financing | Store-only usage |

| Helpful for large renovations | No cashback or travel rewards |

| Easy online & in-store approval | Interest added retroactively if unpaid |

Before applying, it’s important to weigh the advantages and potential drawbacks of the Home Depot Credit Card.

Pros

1. No Annual Fee

You don’t pay an annual membership fee, making it low-risk to keep long-term.

2. 6-Month Special Financing on $299+

Deferred-interest financing helps manage large renovation purchases when they are paid off within the promotional period.

3. Occasional Extended Financing Offers

Special promotions may include 12–24 month financing during seasonal events.

4. Easy Application Process

Online and in-store applications often provide instant decisions.

5. Helpful for Large Home Projects

Ideal for appliances, remodeling materials, flooring, tools, and contractor supplies.

Cons

1. High Variable APR

If you carry a balance beyond the promotional period, interest charges can be significant.

2. Deferred Interest Risk

If the full balance is not paid before the promotional deadline, interest is added retroactively.

3. Store-Only Usage

The card can only be used at Home Depot and its website.

4. No Cashback or Travel Rewards

Unlike general credit cards, this card does not offer ongoing rewards programs.

Overall Summary

The Home Depot Credit Card works best for disciplined borrowers who plan large purchases and can pay them off within the financing window. It is less suitable for those who tend to carry balances long term. If you think you might carry a balance or want broader rewards, consider alternatives like general cashback cards or credit cards with lower ongoing interest rates. Options such as the Citi Double Cash Card or the Chase Freedom Unlimited offer cash back on all purchases and may be more cost-effective if you do not always pay your balance in full. Unlike the Home Depot card, most general cashback cards reward you for every purchase, regardless of retailer, and often provide introductory 0% APR periods for new purchases or balance transfers. They are more versatile for everyday use and can help you save money on interest if you need time to pay down balances. Exploring these types of cards can help ensure you choose the best fit for your financial habits and needs.

Summary of Key Differences:

- Rewards: The Home Depot Credit Card does not offer ongoing cashback, points, or travel rewards, while general cashback cards provide a percentage of cash back on all purchases, no matter the retailer.

- Flexibility: The Home Depot Credit Card can only be used at Home Depot stores and online, while general cashback cards are accepted almost everywhere major credit cards are used.

- Financing: The Home Depot Credit Card specializes in deferred interest promotional financing for large purchases at Home Depot. Most general cashback cards offer an introductory 0% APR for purchases or balance transfers, but do not provide store-specific financing deals.

This means the Home Depot Credit Card is ideal if you prioritize store financing for planned renovations, while a general cashback card is better if you want broader rewards and greater flexibility for day-to-day expenses.

Hard Inquiry Impact on Your Credit Score

When you apply for the Home Depot Credit Card, Citibank performs a hard credit inquiry.

A hard inquiry may:

- Temporarily lower your credit score by 5–10 points.

- Stay on your credit report for up to 24 months.

- Affect approval odds for other credit cards or loans.

However, if approved and used responsibly, the card can:

- Improve your credit mix.

- Help build payment history.

- Increase total available credit (which lowers utilization)

This makes applying worthwhile only if you are confident of approval.

Frequently Asked Questions (FAQ)

Does the Home Depot Credit Card have an annual fee?

No, the Home Depot Credit Card does not charge an annual fee.

What is the minimum purchase required for special financing?

Most promotional financing offers apply to purchases of $299 or more, though terms may vary during special promotions.

Can I use the Home Depot Credit Card anywhere?

No. The card is store-specific and can only be used at The Home Depot retail locations and on its official website.

How long does approval take?

In many cases, applicants receive an instant decision when applying online or in-store. If additional review is required, the decision may take a few days.

Does the Home Depot Credit Card help build credit?

Yes. The card reports payment activity to major credit bureaus. Responsible usage — such as on-time payments and low utilization — can help improve your credit profile.

What happens if I don’t pay off the balance before the promotional period ends?

If the full promotional balance is not paid before the deadline, interest is added retroactively to the original purchase amount from the purchase date. This is known as deferred interest.

Can I increase my credit limit?

You may request a credit limit increase after establishing a positive payment history. Approval depends on your credit profile and financial situation at the time of request.

Is the Home Depot Credit Card Worth It in 2026? (Final Verdict)

The Home Depot Credit Card can be a useful financing tool in 2026 — but its value depends on how you plan to use it.

This store credit card is designed primarily for promotional financing, not for everyday rewards or cashback. If you frequently shop at Home Depot for renovations, appliances, or major home projects, and you pay off balances within promotional periods, the card can help you manage costs without paying interest.

When It Makes Sense

- You make purchases of $299 or more.

- You can pay off the full balance before the promotional deadline.

- You want extra time on returns compared to regular purchases.

- You don’t need cashback or travel rewards from your credit card.

For example, buying a $1,000 appliance with a 6-month special financing plan and paying about $167 per month can help you avoid interest charges, saving money compared to high-interest credit cards.

However, imagine you accidentally miss the deadline and still owe $100 when the 6-month promotional period ends. In this case, interest would be charged retroactively on the entire original $1,000 purchase amount, not just the unpaid $100. With an APR over 25%, you could end up owing an extra $125 or more in interest simply for being a week late. This shows why it is critical to pay the full promotional balance on time in order to truly benefit from the special financing.

When It Might Not Be Worth It

- You tend to carry balances month to month.

- You want a card with rewards for everyday purchases.

- You need a card usable outside Home Depot.

- You don’t shop at Home Depot often.

Because the APR on unpaid balances is high, carrying debt beyond the promotional period can erase any financing benefit.

Final Takeaway

If your goal is project-based financing at Home Depot and you are disciplined with repayment, this card can be a smart tool – especially for planned home upgrades and large purchases. Before you apply, always review your budget and create a clear repayment plan to make sure special financing truly works to your advantage.

If you want broader rewards or use a card everywhere, a general cashback or travel rewards credit card is likely a better long-term choice.

FinovativeHub Editorial Team publishes finance guides, budgeting strategies, credit card reviews, loan insights, and investing content for American readers. Our content is independently researched, fact-checked, and regularly updated using trusted financial institutions, government agencies, and authoritative industry sources. We focus on providing clear, practical, and unbiased information to help readers make smarter financial decisions and build long-term financial confidence.