If you’ve ever looked at your bank account on the 25th of the month and wondered where all your money went, you’re not alone. Millions of Americans struggle with money — not because they don’t earn enough, but because nobody ever taught them how to manage it. That’s where the 50/30/20 rule comes in. It’s simple, flexible, and it actually works in the real world.

In this guide, we’ll break down exactly how to use the 50/30/20 budgeting rule in 2026, walk through real-life examples with real numbers, and show you how to make it work even if your income isn’t perfect or your life doesn’t fit a neat little box.

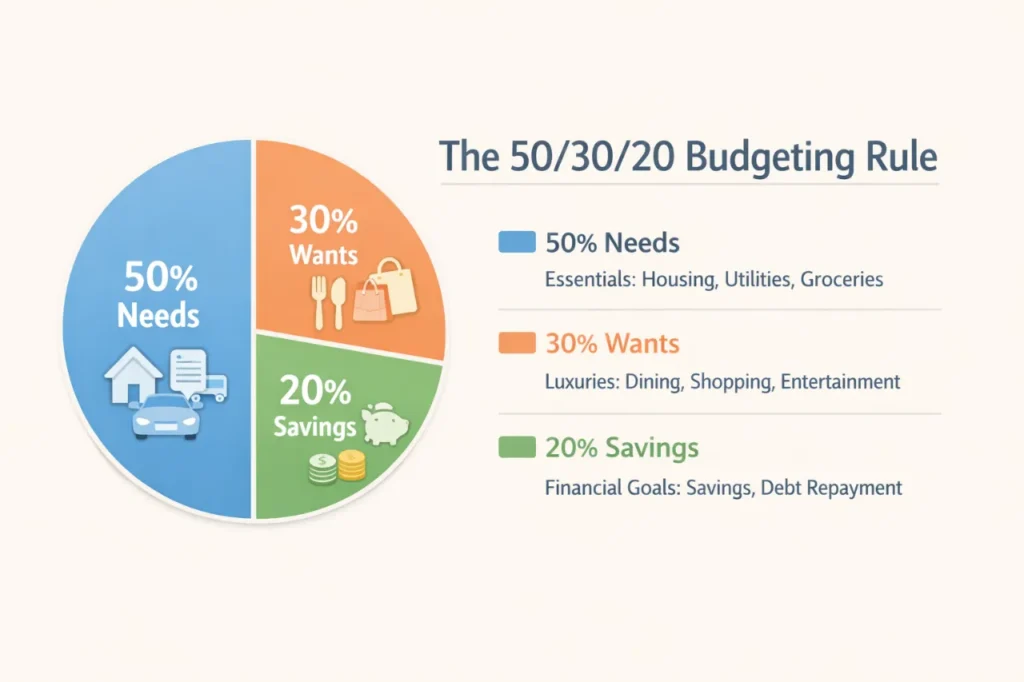

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting framework that divides your after-tax income into three buckets:

- 50% for Needs — rent, groceries, utilities, car payment, insurance

- 30% for Wants — eating out, Netflix, vacations, new clothes you don’t technically need

- 20% for Savings and Debt Repayment — emergency fund, retirement, credit card payoff

That’s it. No 47-category spreadsheet. No color-coded envelope system. Just three buckets.

The rule was popularized by Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, in their 2005 book, All Your Worth. But it’s more relevant now than ever — especially amid inflation, rising rents, and record-high cost of living across the country.

Why the 50/30/20 Rule Still Works in 2026

Let’s be honest — 2026 is expensive. Rent in cities like Austin, Denver, and Nashville has doubled in some areas over the past five years. Groceries cost more. Gas is unpredictable. Student loans are back in repayment. And yet the 50/30/20 rule still holds up because it’s a percentage-based rule, not a dollar-based one. It scales with your income, whether you make $35,000 a year or $135,000.

It also doesn’t shame you for spending on fun. That 30% for wants isn’t a guilty category — it’s built into the budget on purpose. When people feel guilty about every small purchase, they often give up on budgeting entirely. The 50/30/20 rule removes that guilt and replaces it with clarity.

Step 1: Find Your After-Tax Income

Before you can split anything three ways, you need to know your starting number — your take-home pay after taxes, not your gross salary.

Real-life example: Jessica works as a dental hygienist in Columbus, Ohio. She earns $62,000 a year before taxes. After federal income tax, state tax, and Social Security deductions, she takes home about $4,100 per month. That $4,100 is her working number.

If you’re a freelancer or self-employed, this gets a little trickier. Take your average monthly income over the last three to six months and subtract 25-30% for taxes (since taxes aren’t automatically withheld). That’s your after-tax estimate.

If you have side income — DoorDash on weekends, selling on Etsy, occasional overtime — include those amounts, but be conservative. Don’t budget around your best month. Budget around your average month.

Step 2: Calculate Your Three Buckets

Once you have your after-tax income, the math is straightforward.

Using Jessica’s $4,100/month:

| Needs (50%) | 50% | $2,050 |

| Wants (30%) | 30% | $1,230 |

| Savings/Debt (20%) | 20% | $820 |

Simple, right? Now the real question is: what actually goes in each bucket?

The “Needs” Bucket (50%): What Really Counts

Your needs are the expenses that would cause serious problems if you stopped paying them. Think: you’d lose your home, go hungry, or lose your job.

Needs include:

- Rent or mortgage payment

- Utilities (electricity, gas, water)

- Groceries (not restaurant meals — just groceries)

- Health insurance premiums

- Minimum debt payments

- Car payment and car insurance (if you need a car to work)

- Prescription medications

- Childcare or daycare costs

What does NOT count as a need:

- Spotify, Netflix, Hulu

- Gym membership

- Cable TV

- Your daily Starbucks run

- Going out to dinner

Those belong in the wants category. Be honest with yourself here. A lot of people mentally move things from “want” to “need” to make themselves feel better about the budget, but that’s just lying to themselves with extra steps.

Real-life challenge: Marcus lives in Los Angeles and earns $5,500/month after taxes. His 50% for needs is $2,750. But his rent alone is $2,100. That leaves only $650 for groceries, utilities, insurance, and everything else in the needs category. That’s tight — and it’s a reality many people in high-cost cities face.

If your needs exceed 50%, we’ll talk about how to adjust below. But first, let’s look at the other two buckets.

The “Wants” Bucket (30%): Spend Without Guilt.

This is the category that makes the 50/30/20 rule feel human. You’re allowed to spend 30% of your income on things that make your life enjoyable. This is not frivolous — it’s intentional.

Wants include:

- Dining out and takeout

- Streaming services (Netflix, Spotify, Disney+)

- Concerts, sports games, movies

- Vacations and weekend trips

- New clothes beyond the basics

- Hobbies (golf, painting, gaming)

- Gym membership (if it’s optional, not medically necessary)

- Upgraded phone plans

- Amazon impulse buys

Real-life example: Jessica (our $4,100/month example) has a $1,230 wants budget. Here’s what her month looks like:

- Dining out with friends: $180

- Netflix and Hulu: $30

- Weekend road trip: $250

- New running shoes: $120

- Happy hours and coffee: $90

- Concert tickets: $75

- Misc shopping: $110

Total: $855 — she came in under budget and still had a real life.

The key here is awareness. Most people overspend in the wants category, not because they’re irresponsible, but because they don’t track it. Small purchases add up fast. A $6 latte three times a week is $72 a month. That’s not a lecture — that’s just math. Knowing the number lets you decide if it’s worth it.

The “Savings and Debt” Bucket (20%): Your Future Self Will Thank You

This is the most powerful bucket, and it’s also the one most Americans skip entirely. According to recent surveys, roughly 57% of Americans can’t cover a $1,000 emergency from savings. That’s not because people don’t make enough money — it’s because saving has never been made a priority.

The 20% savings bucket includes:

- Emergency fund contributions — aim for 3-6 months of expenses.

- Retirement savings — 401(k), IRA, Roth IRA

- Paying down high-interest debt — credit cards, personal loans (above minimums)

- Saving for specific goals — down payment on a house, new car, kids’ college fund

Real-life example: David is a 28-year-old teacher in Chicago making $3,800/month after taxes. His 20% savings are $760/month. He breaks it down like this:

- $300 to his Roth IRA (auto-transferred on payday)

- $200 to his emergency fund

- $260 as an extra payment on his $14,000 credit card debt

He’s not getting rich overnight, but in 12 months he’ll have $2,400 added to his emergency fund, $3,600 contributed to retirement, and knocked $3,120 off extra credit card payments — potentially saving him thousands in interest.

Pro tip: Automate this bucket first. Set up automatic transfers on payday so the money moves before you even see it. What you don’t see, you don’t spend.

What to Do When the Numbers Don’t Add Up

Here’s the thing — for a lot of people, the math doesn’t work perfectly at first. If you live in a high-cost city, have student loans, or are a single-income household, your needs might eat up 60% or even 65% of your take-home pay.

That’s okay. The 50/30/20 rule is a target, not a rigid law.

When needs exceed 50%, here’s what to do:

Option 1: Trim your wants. Instead of 30% on wants, drop to 20% or even 15%. Redirect the difference to cover your needs overage and still protect your savings.

Option 2: Increase your income. This is easier said than done, but even a part-time gig — $400 extra a month — can significantly change the math.

Option 3: Audit your “needs.” Sometimes things we’ve labeled as needs are actually wants. Do you really need unlimited wireless data? Could you cook more and spend less on groceries? Small cuts inside the needs category add up.

Option 4: Play a longer game. If you’re paying down debt aggressively right now, it’s acceptable to temporarily drop your savings percentage to 10% while you knock out high-interest debt. Once it’s gone, redirect that payment into savings.

How to Track Your Budget in 2026

You don’t need a fancy app — but having one helps. Here are some popular free and low-cost tools Americans use right now:

- YNAB (You Need A Budget) — $14.99/month, but very powerful for zero-based budgeting

- Mint — free, connects to your bank accounts automatically.

- Every Dollar — Dave Ramsey’s free budgeting app

- Google Sheets or Excel — the old-fashioned way, but it works great if you build a simple template.

- Your bank’s built-in tools — Chase, Bank of America, and many others have spending category trackers built right in

Whatever tool you use, review your budget once a week, even for just 5 minutes. Sunday evening is a good time. Look at what you spent, see where you are in each bucket, and make a quick plan for the week ahead.

Real-Life 50/30/20 Budget Example: A Full Month

Let’s walk through a complete example. Meet Sarah, 32, living in Nashville, Tennessee. She works in marketing and brings home $4,600/month after taxes.

Sarah’s 50/30/20 Budget:

Needs ($2,300 / 50%)

- Rent: $1,350

- Groceries: $320

- Utilities + Internet: $150

- Car insurance: $110

- Health insurance: $200

- Minimum credit card payment: $75

- Gas: $95 Total: $2,300

Wants ($1,380 / 30%)

- Dining out: $200

- Streaming services: $45

- Gym: $40

- Shopping and clothing: $150

- Weekend activities: $225

- Hair and personal care: $80

- Vacation savings jar: $300

- Miscellaneous fun: $100

- Coffee and snacks out: $90

- Books and entertainment: $150 Total: $1,380

Savings & Debt ($920 / 20%)

- Roth IRA contribution: $400

- Emergency fund: $300

- Extra credit card payment: $220 Total: $920

Sarah isn’t wealthy. She’s not driving a luxury car or living in a penthouse. But she’s building real wealth, living a real life, and not stressed every time she checks her bank balance.

Common 50/30/20 Mistakes to Avoid

Mistake #1: Using gross income instead of net income. Always work with what actually hits your bank account, not your pre-tax salary.

Mistake #2: Forgetting irregular expenses. Car registration, annual subscriptions, holiday gifts, and back-to-school costs are real expenses. Divide them by 12 and include them monthly.

Mistake #3: Never revisiting the budget. Life changes. You get a raise. Rent goes up. A kid arrives. Revisit your 50/30/20 split at least every six months.

Mistake #4: Giving up after one bad month. Going over budget in one category for one month doesn’t mean the whole system failed. It means you’re human. Just adjust and keep going.

Mistake #5: Not paying yourself first. Savings should come out at the top, not whatever is “left over” at the end of the month. There is rarely anything left over.

Final Thoughts: Your Budget Is a Tool, Not a Punishment

Budgeting isn’t about restricting your life. It’s about making intentional choices with your money so your money doesn’t control you. The 50/30/20 rule gives you structure without making you feel like you’re in financial prison.

Start this week. Look at your last two months of bank statements. Categorize every expense into needs, wants, or savings. See where you actually are. Then decide where you want to be.

You don’t have to be perfect. You just have to be intentional.

And in 2026, with everything costing more than it did a few years ago, being intentional with your money isn’t just smart — it’s essential.

What is the 50/30/20 rule?

A budgeting framework that splits your after-tax income: 50% for needs, 30% for wants, and 20% for savings and debt payoff.

Does the 50/30/20 rule work for low incomes?

Yes — it’s percentage-based, so it scales with any income level. The hardest part for low earners is keeping needs under 50% in high-cost cities.

What counts as a “need” in the 50/30/20 rule?

Rent or mortgage, utilities, groceries, minimum debt payments, health insurance, and transportation required for work.

Have questions about making the 50/30/20 rule work for your specific situation? Drop them in the comments below. Every financial situation is different, and there’s no shame in asking.

“Read full guide: Personal Finance in 2026”

FinovativeHub Editorial Team publishes finance guides, budgeting strategies, credit card reviews, loan insights, and investing content for American readers. Our content is independently researched, fact-checked, and regularly updated using trusted financial institutions, government agencies, and authoritative industry sources. We focus on providing clear, practical, and unbiased information to help readers make smarter financial decisions and build long-term financial confidence.